This is a new page, posted on 12/4/2025. This webpage consists of two subchapters from my FERSGUIDE presented here for free, to try and educate folks as to why no one over the age of 59 1/2 should have a TSP account, and for those younger than 59 1/2, to move the majority of their funds away from the TSP.

Tell Me How Bad the “New” TSP Is!

Anyone that has logged into the TSP website since May 26, 2022, knows that Converge was not an advancement. Converge is the name given by the TSP to the contract with Accenture Federal Services (AFS) to “upgrade” and maintain the TSP records and accounts. You can read the 100-page contract here[1]. Don’t try and figure out how much this mess cost the Federal Retirement Thrift Investment Board (FRTIB), as the contract copy released does not show any dollar amounts. Numerous FOIA requests have been made to the FRTIB requesting a copy that shows the total amount spent with AFS under the contract. The FRTIB maintains that they do not have to release the contract with dollar amounts showing. How’s that for a “sunshine law?” What are you hiding? What are you embarrassed about?

As many of you know, I have been authoring the FERSGUIDE for over 25 years. I receive many comments from readers and past subscribers. Many of you have shared your frustrations with the new TSP with me. It’s been bad from the start.

Someone had the bright idea to remove all the historical statements from the TSP website! All you will find there now are statements after May 26, 2022. Can you imagine that? All the historical information that we used to be able to login and print off, is gone. Just gone. I’m not an “IT guy,” but I know one thing about the IT world, and that is “storage is cheap.” Storing data is not nearly as expensive as it used to be. I can’t imagine why AFS thought that removing all historical data was a good idea. “What if I need a historical statement?” That’s easy – just call the ThriftLine and wait three months. That’s what my divorce clients must do. The best part is that when the statement finally arrives, it looks like a faxed copy of a fax, in terms of print quality.

“Well, okay…..it could be worse than not having statements, I just need to know my balance on a certain date? Well, you’re out of luck there as well. On the old website, you could pull up your account balance on any stated date for the most-recent 20 years or so. All of that is gone. The TSP has loaded some year-end balances, but just for that date, and that date alone. The only way to ascertain a TSP balance on a date certain is to begin with quarter-end share balances for the quarter prior to the date in question, and then apply all transactional items, such as contributions, loan payments and interfund transfers, up to the desired date. Then, re-price that number of shares at the daily share price for that date. When a federal employee gets married after their hire date, that creates a premarital TSP balance that must be segregated out. Since about half of the population will go through a divorce, this is a big issue, and one that AFS obviously did not consider when designing the new system. Many times, we must review 10-20 years of statements and identify all interfund transfers executed during the marriage.

Now, with the number of shares known, it’s time to re-price those shares on the desired date. When you request a share price on a stated date on the website, the resultant share price result is displayed with two digits to the right of the decimal, yet TSP share prices are valued at four places to the right of the decimal. Another AFS mistake.

Those of you who are already taking monthly payments based upon your life expectancy, may have noticed that your payment amount changed after Converge. That’s because under a life-expectancy payment plan, the payment is a function of your December 31 balance of the prior year multiplied by a factor that determines your monthly payment. Because the TSP seemingly has no history before May 26, 2022, the TSP recalculated the monthly payment using the May 26, 2022, balances. That means the TSP will have to make a payment adjustment (up or down) before December 31, to all life-expectancy payment participants so that the proper amount required under IRC 72(t) is paid out by December 31. If an incorrect amount is paid, then the 10% penalty comes into play for ALL payments under that life-expectancy payment stream.

One of the new products touted by the TSP stemming from Converge was the addition of a Mutual Fund Window (MFW). The fees for the MFW are staggeringly high. The annual “maintenance fee” just to have a MFW is $132. Each trade is $28.75 within the same fund family and $57.50 per trade between fund families. Although this was a feature desired by participants, it is my opinion that the high fee schedule is thwarting participation. The latest MFW metrics from the August 2025 FRTIB board meeting minutes indicate just about 7,500 MFWs opened out of 7,255,246 accounts, or .0010337 (that’s just over one-tenth of 1%) of all TSP participants. That number may grow, but I personally do not believe it will enjoy a wide participation rate due to the high fees.

From my 25+ years at this, I can tell you what TSP participants want more than anything. They want the ability to make a withdrawal and specify the fund(s) that should be sold to fund the withdrawal. The TSP’s own 2022 Gallup poll indicated that 89% of TSP participants desire the ability to specify from which investment funds should be withdrawn from. Simple as that. What do we get instead? An expensive MFW with a poor participation rate.

“C’mon, Dan, you’re making this up, right? No “upgrade” can be that bad, right?” Unfortunately, it’s all true. As I always say to the TSP – “Go ahead, sue me. It’s all true.”

The Converge Project also had a significant negative impact on the processing of the court orders used to divide TSP account balances in divorce. Comments on that part of Converge can be found in Chapter 4.1.6.

All we got out of Converge was a MFW that no one uses and an app that has not been well received. No other new functionality was added. I’ll bet a dollar that not one person on the AFS development team is a former federal employee with a TSP account.

If you are an onboard employee, then you are stuck with the TSP, so max out your contributions and make the best of the situation.

If you are an annuitant who has attained the age of 59½, I can’t think of a single reason to be at the TSP. You wouldn’t put up with this level of service from any other service provider in your life – so why would you put up with it from the TSP?

Consider moving your money into an IRA and leaving $200 on deposit at the TSP, just in case you ever want back into the G fund, as that is somewhat unique to the TSP.

Chris Barfield has moved his TSP account to an IRA, and in doing so, he created this useful article, “TSP to IRA Transfer: A How To”[1], to walk you through the steps.

In May 2023, I moved my TSP account balance to Charles Schwab and I am delighted with every aspect of my Charles Schwab account. I can invest in anything that I want to, but even if I just want to mirror the TSP funds, the fees at Charles Schwab for the same index funds are lower.

In mid-2023, I penned an “Open Letter to the TSP[2]” and Chris Barfield has been kind enough to host that letter on his website. Please take the time to read it and question why Congress has allowed the TSP to move so far away from its roots. An agency that used to brag about printing on both sides of the mailed paper statements to save on postage charges three to four times the fees that Fidelity charges on identical mutual funds.

I frequently receive emails from readers which share their nightmare interactions with the “new” TSP. I simply can’t make this stuff up. The text in italics is quoted directly, in its entirety, from the email sent to me. This is just one of many, but demonstrative of the message. This poor guy is trying to do the right thing and leave the TSP, and even that does not go well.

“Thanks again for making my retirement a smooth success. I have been (attempting) to transition my TSP accounts, both Traditional and Roth, to very well managed and low fee IRAs. So, with my advisor we started the process:

July 27: first call with TSP and financial advisor. Was told there was a one-week security period so call back the following week. Fine.

August 3: second call after the one-week security waiting period. Everything went fine. Decided to leave $1,000 in each account to keep the TSP accounts open. All information was provided and confirmed and the checks would be sent out and received within 10-14 days directly to the financial advisor company accounts. Checks!

August 24: after 3 weeks I called TSP to ask wtf is going on and where’s my checks? I was immediately told there was a “glitch in the systems and they were just notified today.” I said fix and send the checks. I was advised they couldn’t do that and had to start all over.

August 30: my advisor and I contacted TSP again and was advised there was no “glitch” she had ever heard of that was absolutely false. We were then told that since my wife is the beneficiary of the TSP she would have to agree to the funds transfers and electronically sign a document which would take several days to prepare. Once that was signed, the funds could be transferred.

Sept 4: electronic documents received , signed, returned by beneficiary.

Sept 22: only 1 check arrived, the traditional TSP funds. I called and asked why the Roth had not been received. Was told they would check on it, but then stated they realized TSP can only do one account transfer at a time. I told them to proceed with the Roth immediately, which they agreed.

Sept 29: I called TSP again and asked what the status was. After going over all the details to send the Roth check out to my advisor, at the very end I was told TSP couldn’t make the transfer. The policy, the nice gentleman said, was there was a 30-day waiting period between transferring account from TSP. What?

Every call with TSP there is new and different information provided. I cannot believe they handle the largest financial retirement program around. What a %#$& show. Now I can’t even get my money until late October. I started this in July ! Is this common? Even my financial advisor said something isn’t right but we have no recourse. Incredibly disappointed.”

Hey TSP – sue me! It’s all true.

Tell Me How the TSP’s Fees have Increased

I was hired into federal employment in 1992. One of the first things touted to me by the “old timers” was that I needed to invest as much as I could into the TSP. True. I was also told by those same folks, and by the TSP, that the TSP’s expense ratios were low. Not true anymore. Maybe back 30 years ago, but it is no longer the case.

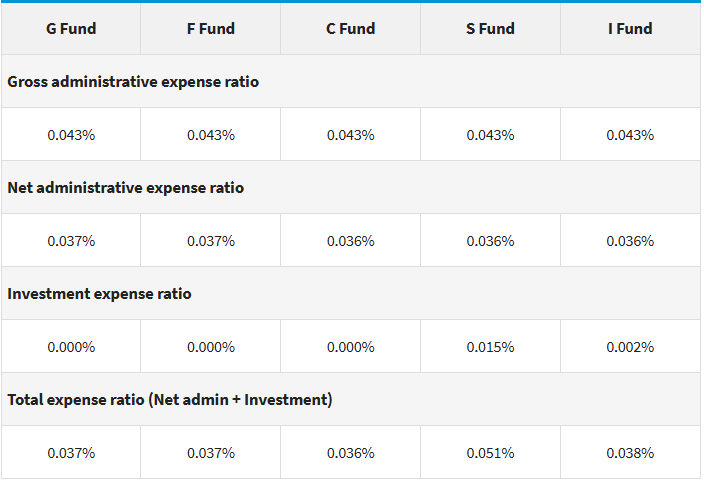

The graphic below shows the TSP’s expense ratios for 2024:

Look at the C fund. That is 3.6 basis points. That’s 36 cents per $1,000 invested.

Now, let’s’ look at Fidelity’s FXAIX mutual fund[2], the “Fidelity® 500 Index Fund.” That fund has an expense ratio of .015%, or 1.5 basis points. That’s 15 cents per $1,000 invested. That puts the C fund expense ratio almost 2.5 times the expense ratio of the same fund type at Fidelity.

Look at the S fund. That is 5.1 basis points. That’s 51 cents per $1,000 invested.

Now, let’s’ look at Fidelity’s FNCMX mutual fund[3], the “Fidelity® NASDAQ Composite Index® Fund.” That fund has an expense ratio of .029%, or 2.9 basis points. That’s 29 cents per $1,000 invested. That puts the S fund at 1.75 times higher than the expense ratio of a similar fund at Fidelity.

The TSP’s expenses on those two funds together average TWICE the expenses of a similar fund at Fidelity. I have no money at Fidelity. I just picked Fidelity because they are well known, and I know they offer low-cost mutual fund investments.

Even the TSP’s own materials state:

“Costs are important in saving for your retirement. Even small differences in expenses can, over time, have a dramatic effect on a fund’s performance and the size of your account.”

Just another reason for annuitants over the age of 59½ to consider moving their TSP balance to a lower-cost custodian and lower-cost products.

I’m not a big fan of the TSP for annuitants. If you are taking distributions penalty-free under the “age 55” rule, then I understand the need to leave some funds at the TSP to cover those penalty-free distributions. As mentioned earlier in this section, that does not preclude you from moving most of your funds out of the TSP into an IRA.

Chris Barfield’s take can be found in his article “TSP – Should I Stay or Should I Go?[1]”

If you are age 59½, I can’t think of a single reason to keep your funds at the TSP, but I can think of many reasons to not keep your funds at the TSP as an annuitant over the age of 59½:

1) If you are a married participant, every single time you request a distribution, you must obtain your spouse’s consent. What a PITA. You will not have that issue with an IRA custodian. The TSP does this because that’s how they interpret the Spouse Equity Act.

2) Trading is difficult and not real-time by any means, as your InterFund Transfer must placed before noon EST for an end-of-day trade.

3) You are limited to two InterFund Transfers per month.

4) The website is dreadful.

5) You still can’t direct the TSP as to which fund(s) you’d like your distribution to be funded from.

6) The TSP will not withhold state taxes and has limited federal tax options.

7) There are only five underlying core funds.

8) You can’t add any funds to the TSP after you retire.

9) Distributions are not immediate.

It’s what you’d expect when you cross a federal agency with a financial-services firm. A donkey.